Navigating the Challenges: Wages and Reforms in Madagascar's Economy. Part Sixteen - Personal Tax Reform

Current Personal Tax System in Madagascar

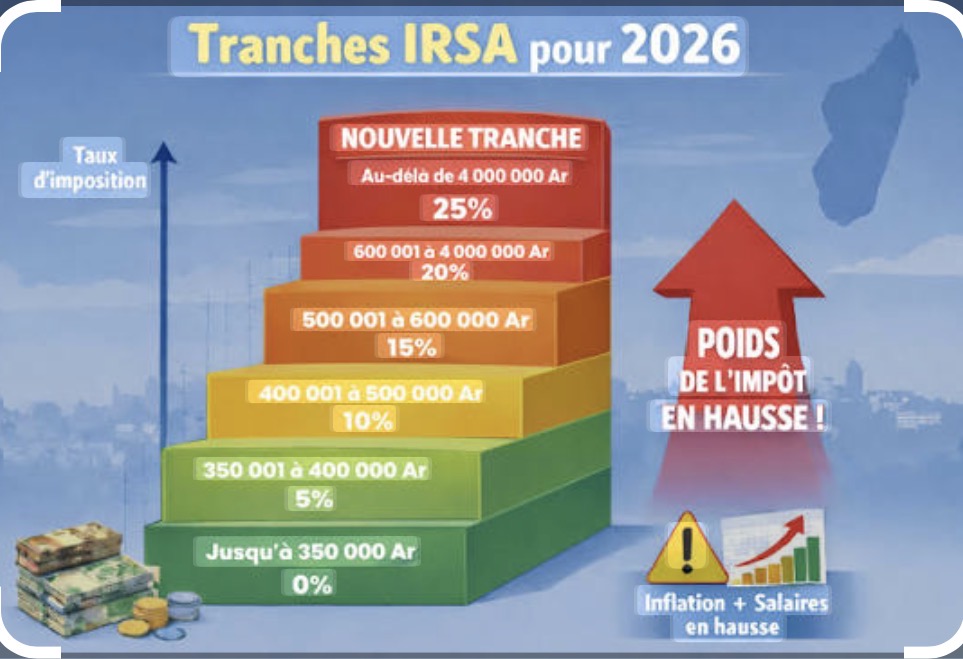

1. Tax Brackets:

- 0% for income up to MGA 350,000 per month

- 5% on income from MGA 350,001 to MGA 600,000

- 10% on income from MGA 600,001 to MGA 1,200,000

- 15% on income from MGA 1,200,001 to MGA 2,000,000

- 20% on income from MGA 2,000,001 to MGA 4,000,000

- 25% on income above MGA 4,000,000 (recently proposed but not uniformly implemented yet)

2. Tax Collection:

- Approximately 10.4% of GDP is collected through taxes, indicating a narrow tax base and reliance on indirect taxes.

3. Challenges:

- High levels of tax evasion, especially in the informal sector.

- Limited administrative capacity to enforce and collect taxes effectively.

- The system is perceived as complex and difficult to navigate for many taxpayers.

Proposed Improved Tax System

1. Broaden the Tax Base:

- Reduce exemptions and streamline the tax code to ensure more individuals and businesses are captured in the tax net, particularly in the informal sector.

2. Enhanced Progressivity:

- Maintain the 0% tax rate for low-income earners but ensure that higher income brackets are more effectively taxed. Implement the 25% rate for very high earners consistently to improve equity.

3. Simplification and Clarity:

- Streamline tax forms and processes to make it easier for taxpayers to comply. This could include clearer guidelines and a more user-friendly online tax filing system.

4. Strengthening Enforcement:

- Invest in training tax officials and improving technology for better tracking of income and tax compliance. Employ data analytics to identify potential tax evaders.

5. Public Awareness Campaigns:

- Educate citizens about the importance of taxes in funding public services, thereby increasing compliance and reducing resistance to tax reforms.

6.Use of Revenue for Public Services:

- Allocate additional tax revenues to improve healthcare, education, and infrastructure, making the benefits of taxation visible to the public to promote compliance and trust in government.

Current Yield from Personal Income Tax

The yield from personal income tax in Madagascar is challenging to quantify precisely due to the informal economy and collection inefficiencies. However, it is a significant part of the overall tax revenue. The specific contribution of personal income tax to total tax revenue can vary, but generally, it is lower than that of VAT and other indirect taxes.

Potential Impact of Proposed Changes on Tax Revenue

1. Broaden the Tax Base:

- By reducing exemptions and increasing compliance among informal sector workers, the government could significantly increase the number of taxpayers. This could potentially add millions of Ariary to the tax base.

2. Enhance Progressivity:

- Implementing the 25% tax bracket for high earners could yield substantial revenue. If we estimate that a small percentage of the population (one per cent ) falls into this category, it could generate additional revenue in the hundreds of millions of Ariary.

3. Simplification and Clarity:

- Streamlining processes could improve compliance rates by 10-20%. If compliance increases from 60% to 70%, this could yield an additional boost to tax revenues.

4. Strengthening Enforcement:

- Improved enforcement and use of technology could reduce tax evasion by an estimated 15-30%, which would directly increase tax revenues depending on the current evasion rate.

5. Public Awareness Campaigns:

- Educating the public about the importance of taxes could improve compliance further, potentially increasing tax revenues by an additional 5-10%.

Estimated Revenue Increase

While precise figures are difficult without specific data, a well-implemented reform package could potentially increase personal income tax revenue by 20-50% over time, depending on the effectiveness of the measures. For example, if the current yield from personal income tax is estimated at MGA 200 billion, reforms could potentially increase this to between MGA 240 billion and MGA 300 billion annually, depending on the scale of compliance improvements and the increase in taxable income due to broader coverage.

The proposed reforms in Madagascar's personal income tax system could yield significant increases in tax revenue by broadening the tax base, enhancing progressivity, and improving compliance. The overall impact would depend on the successful implementation of these reforms and the ability to enforce tax laws effectively.

Comments

Post a Comment